Table of Contents

What are the different Methods of Valuation?

What is Business Valuation?

Business valuation is a process of evaluating a company’s monetary (or better say economic) worth. It’s used in the determination of a company’s sale value, in establishing partner ownership, mergers and acquisitions, strategic planning, equity financing, debt financing, litigation and dispute resolution, etc. This involves assessing assets, and liabilities, forecasting revenue, expenses, cash flows, etc.

Valuation analysts use a range of methods to estimate a business’s value, focusing on its future earnings potential for assessing its worth.

Today, we shall discuss a few of the popular valuation methods in this article. But before that let’s understand why valuation is required and what’s the need to master this craft!

Table of Contents

Importance of Valuation

If you’re here, you might have heard of the popular show Shark Tank India, and the significance company valuation holds. Even after having an amazing product, many founders failed to grab a deal because of an incorrect or hyped valuation!

Valuing a business isn’t simply an abstract exercise; instead, it plays a pivotal role in varied business use cases and guides them while making crucial decisions.

Why do we need Business Valuation?

Here is the list of reasons why we need business valuation-

- Buying/ Selling: It serves as the compass that initiates the talk of negotiations while ensuring fair deals for both parties.

- Investment Planning: Every investment decision is nothing but valuation in disguise, which helps determine what kind of project enhances the company’s value and which one is purely a lemon deal.

- Mergers and Acquisitions: Valuation, an indispensable tool during mergers or acquisitions, aids stakeholders in navigating through the complexities of consolidation.

- Onboarding Investors: Investors need assurance of the company’s worth before committing funds, making valuation a prerequisite for attracting capital. Determining ownership percentages and equity distribution mandates accurate valuation.

- Employee Compensation: Business Valuation is required to determine the value of company shares allocated to employees as part of an ESOP. This process ensures a fair distribution of ownership and benefits among employees.

- Exit Strategy: For entrepreneurs looking to exit, a true valuation model provides a fair price for years of effort and dedication.

- Tax Mandates: Valuations are required for tax purposes to ensure compliance with regulatory frameworks and fair assessment of tax liabilities.

- Personal Matters: Valuation provides clarity, especially in the case of restructuring partnerships or divorce issues on partnership arrangements and asset distribution, respectively.

What are the different Methods of Valuation?

Deep dive into the comprehensive analysis of various business valuation methodologies and their pros and cons.

1. Discounted Cash Flow

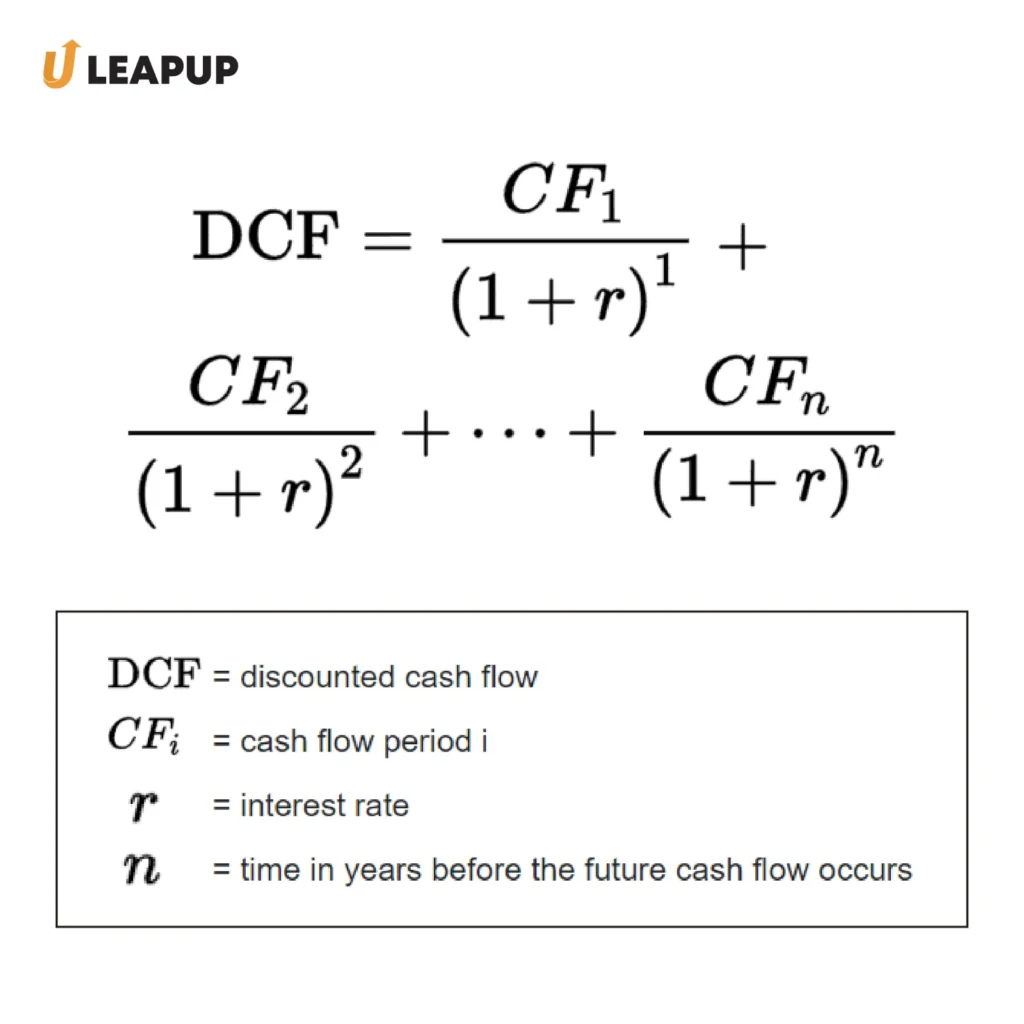

What is DCF?

Discounted Cash Flow (DCF) analysis is useful in determining the intrinsic value of an entity by estimating the present value of its expected future cash flows while taking risk into account. It relies on the principle that the value of a business is the sum of all its future cash flows, discounted to their present value.

DCF model stands on three pillars: Cash Flows, Growth, and Risk.

Pros:

- Comprehensive Analysis Tool: Gives a thorough analysis of an entity’s value by considering its future cash flows.

- Widely Accepted: Regarded as a standard and widely accepted approach in estimating valuations, making it feasible for investors to compare and comprehend different opportunities.

- Versatility: DCF can accommodate various business scenarios by adjusting input assumptions such as discounting factor, and growth rate.

Cons:

- Reliance on Variable Inputs: Heavy reliance on forecasts and variable inputs such as growth rates and discount rates might lead to inaccuracies because of uncertain assumptions.

- Susceptibility to Manipulation: Susceptible to modulation and manipulation for producing more favorable forecasts, especially by changing input assumptions.

- Preference for Certain Industries: DCF valuation tends to favor industries with consistent growth patterns or those with easily predictable trends, making it less suitable for companies with uncertain cash flows.

- Minor adjustments in the projected growth rate or cost of capital can have a disproportionate effect on the calculations, i.e. it is highly sensitive to inputs.

- Minor variations in growth rate and cost of capital can significantly impact valuation.

DCF Utilizes future cash flows adjusted for inflation to determine business value. Free cash flows are emphasized as the key value driver. Relies on projecting discounted FCF using WACC, growth rate, and perpetual growth rate.

Take for instance, suppose a company expects to generate $4 million in free cash flow annually for the next 10 years. Using a discount rate of 12%, the present value of these cash flows would be calculated to arrive at the business valuation

2. Comparable Company Analysis

Comparable Company Analysis (CCA) is also known as trading multiples or relative valuation methodology which is used to derive an entity’s value by comparing it to similar publicly traded companies. It involves examining various financial metrics and valuation multiples of comparable companies within the same sector or industry to fetch the target company’s value.

Here, we are going to talk about the two most commonly used multiples availed within the framework of CCA for assessing a company’s value- Revenue Multiple and EBITDA Multiple.

• EBITDA Multiple

The EBITDA (Earnings Before Interest, Taxes, Depreciation, and Amortization) method of business valuation is quite simple. It is calculated by multiplying current EBITDA by an agreed-upon multiplier, resulting in a quick estimate of the entity’s worth.

Pros:

- It is an easy and elegant method of company valuation.

- Widely used because of its simplicity, even by critics.

- At times, it acts as a benchmark for negotiations between buying and selling parties.

Cons:

- Might not be able to capture every nuance of business, due to its oversimplification.

- Heavy reliance on Multipliers, which vary depending on the business scenarios.

To understand better, say a company has an EBITDA of 20 million and the agreed-upon multiplier is 7, then the valuation as per this method would be 140 million.

• Revenue Multiple

The Revenue Model Method of Valuation assesses a business’s worth by applying a multiplier to its total sales. It serves as an alternative to the EBITDA Multiple method, especially when EBITDA is negative or unavailable.

Pros:

- Similar to EBITDA Multiple but applicable in cases where EBITDA is unavailable or negative.

- It focuses on total sales, which can be a crucial benchmark for certain industries.

Cons:

- Like the EBITDA Multiple, it may oversimplify valuation and overlook specific business factors.

- Reliance on total sales as a benchmark may not fully capture the financial health of a business.

Let’s understand with an example, say If a company’s annual revenue is $5 million and the industry-standard multiplier is 2, the valuation would be $10 million.

3. Precedent Transactions

The Precedent Transactions business valuation method derives the worth by analyzing comparable transactions within the industry. It avails multiples such as net income or EBITDA for calculation. This method acts more as a market barometer than a strict approach for estimating valuations.

PE firms often use Precedent transactions in the case of valuing startups by identifying recent transactions similar to the target company in terms of business model, industry, growth stage, and other such factors. These transactions can be investments, mergers, and acquisitions.

Mainly, this methodology proves quite useful when market multiples are not present.

Pros:

- Less calculative than DCF as it is based on comparable transactions within the industry.

- Provides insights into valuation benchmarks and trends in the market.

- As mentioned earlier, it indicates market sentiments of similar companies in the sector.

Cons:

- Since it’s based upon other transactions in the industry, finding true comparables is essential and a bit difficult too.

- Every business has a unique aspect, which it may not accurately reflect.

- More of a barometer than a precise valuation approach.

4. Asset-Based Valuation

Asset-based valuation is a method where company valuation is assessed by its net assets or liquidation value. This is mainly suitable for asset-rich yet low-profit-making entities.

For instance, a furniture business determines its value by its furniture inventory, property, and related equipment.

This method of business valuation opts for a bottom-up approach, where a business is valued as a sum of its parts, focusing on assets like inventory, machinery, intellectual property, and goodwill. It fits fine in the asset-rich sectors, such as furniture stores, construction, vehicle rentals, etc.

There are two main approaches to this valuation methodology-

- Going Concern Asset-Based Approach

- Liquidation Value Approach

• Going Concern Asset-Based Approach

Under this methodology, the company’s operations are assumed to be a going concern.

The value of a company is derived by reducing its liabilities from the fair market value of its assets.

Pros:

- Reflects the ongoing operation of the business.

- Useful for companies with stable operations and positive cash flows.

- Takes into account the value of intangible assets like brand reputation and customer relationships.

- Useful for cyclical businesses, provides clarity amidst market fluctuations.

- Supported with asset valuations and depreciation schedules.

Cons:

- May not reflect the true market value of assets if they are outdated or overvalued on the balance sheet.

- Can be intricate, especially with different assets at different stages of the life cycle.

- Doesn’t consider potential changes in market conditions or future earnings potential.

- Relies heavily on the accuracy of asset valuation, which can be subjective.

- Can’t be used as a sole methodology even in an asset-rich business. A basic grasp of other business valuation methods is required to give a complete picture. However, sometimes it is the option left to value a business

• Liquidation Value Approach

This method assesses the value of a business as if it were to be liquidated, i.e., if its assets were sold off and liabilities paid off. The liquidation Value approach assumes that an entity is not a going concern and focuses on the immediate sale value of its assets.

Pros:

- Presents a conservative estimate of value, as it considers the worst-case scenario.

- This method is particularly useful for distressed companies or those with significant tangible assets that can be easily liquidated.

- Helps investors and creditors understand the minimum value they might realize in case of liquidation.

Cons:

- As the name suggests, this method ignores the value of intangible assets like brand reputation and intellectual property, because the entity isn’t assumed going concern, hence the intangible assets don’t hold that worth.

- It is assumed that the assets can be sold quickly, which is not always the case, and which further delays liability payback.

- At times, the Liquidation approach ends up undervaluing a company especially if the market value of assets exceeds its book value.

5. Real Option Analysis

This method sees companies as a compilation of real options. It allows for the valuation of strategic opportunities beyond traditional means.

In Real Option Analysis, Valuation analysts assess the value of a company by considering uncertainties and potential market changes.

Essentially, the Real Option Valuation Method provides a framework for valuing flexibility and strategic choices in an uncertain environment, be it for an entire company or a specific project within that company.

For instance, it can be used by a mineral exploration firm for estimating various exploration projects based on potential outcomes, which can aid in strategic investment decisions amidst uncertain geological conditions. On the other hand, a mature consumer goods industry or low-tech manufacturing business might not opt for it.

Pros:

- A subtle methodology of valuation specifically for companies facing uncertain futures.

- It considers a range of real options, giving a 360-degree view of the potential value.

- Endorsed by top B-schools and leading consulting firms due to its depth of analysis.

Cons:

- Due to its intricate nature, real Option analysis is less likely to be adopted as an approach to business valuation.

- Requires a thorough analysis of a company’s strategic options.

- Companies with straightforward revenue streams are less likely to adopt it (due to the work involved)

Summing Up!

As Professor Ashwath Damodaran says, Valuation isn’t just about numbers, but a craft that requires patience and practice. It is a map that can help business owners make informed decisions and bank into untapped potential.

There are many methods for valuing a company. Selecting the correct valuation method depends on various factors such as industry and the growth potential of a business.

Do you wish to learn this craft? If yes, then check out our comprehensive Financial Modelling and Valuations program.

Even if you are not ready to get your hands in the nitty gritty of valuations, you can still register for the latest webinar

“Career in Finance” which answers every imaginable query in the field. (and yes, it’s free!!!)

Till then, Happy FinUpskilling:)

-

shaswat srivastava

- No Comments

- Hemat Khatri

Student